Hidden fees and unexpected delays can turn a simple OctaFX withdrawal into a costly mistake. Depending on your method and timing, a $1,000 withdrawal may lose $15–40, and weekend requests often face extra charges or slower approval.

While OctaFX maintains strong success rates for verified accounts, traders still worry about missed details.

This 2025 guide uncovers every visible and hidden cost, offers time-of-day optimization tips, includes an interactive calculator, and addresses common withdrawal problems rarely covered elsewhere.

Can You Trust the OctaFX Withdrawal Process?

Traders often fear account freezes, sudden document rejections, or hidden limits.

The reality: OctaFX processes over 96% of withdrawal requests for fully verified accounts, with most failures linked to incomplete KYC steps or flagged trading patterns—not arbitrary denials.

OctaFX operates under SVGFSA regulation (License No. 21947). While this offshore oversight isn’t as strict as EU or ASIC standards, it does enforce structured approval workflows, meaning each rejection carries a documented reason.

The simplest way to avoid delays?

Complete full verification before your first withdrawal. Doing so minimizes the risk of rejection and puts your request in the same success bracket as the vast majority of traders.

Complete Withdrawal Fees Table (Updated January 2025)

Below is a transparent breakdown of OctaFX withdrawal costs, including broker commissions, processor fees, hidden charges, and processing times. Use this to estimate your net amount on a $1,000 withdrawal.

| Method | Broker Fee | Processor Fee | Hidden Costs | Total ($1,000) | Time | Limits | Notes / Best For |

|---|---|---|---|---|---|---|---|

| Bank Transfer | $20–30 | $20–40 | Receiving bank charges + 2–4% currency conversion if non-USD | $60–100 | 1–5 business days | $50–10,000 | Best for larger withdrawals at lowest % cost. Slower on weekends; full KYC required. |

| E-wallet | $10–20 | $5–10 | FX conversion if non-USD | $20–40 | 24–48 hrs | $20–5,000 | Good balance of speed + reliability. Regional availability (India, Nigeria, Malaysia). Verified accounts clear fastest. |

| Crypto | $5–10 | $5–15 | Blockchain fee, ±1–3% volatility risk | $15–35 | <1 hr | $10–2,000 | Fastest method, ideal for small tech-savvy withdrawals. Value depends on crypto price at transfer. |

Hidden Costs & Withdrawal Timing (Updated January 2025)

TL;DR — Key Insights

- Currency conversion spreads (2–4%) = $20–40 lost on a $1,000 withdrawal in non-USD.

- Weekend/holiday delays = +48–72 hrs if submitted late Friday.

- Verification gaps = #1 rejection cause.

Most Common Issues (Affect Most Users)

| Issue | Why It Happens | User Impact | How to Avoid |

|---|---|---|---|

| Currency Conversion (2–4%) | Account ≠ withdrawal currency | $20–40 cut on $1,000 | Keep account in USD/EUR, or withdraw in same currency |

| Weekend/Holiday Delays | Banking networks pause settlement | Friday PM requests processed Monday | Submit before Fri 3–4 PM local time |

| Verification (KYC) | Expired/missing documents | Request rejected until resubmission | Keep ID + proof of funds updated |

Less Common but Significant

- Dormant Account Fees → Balance cut if inactive. Check dormancy rules before withdrawing.

- Bank Detail Mismatches → Name/number errors = delays. Always cross-check spelling.

Rare Edge Cases

- Regulatory Holds → Extra compliance reviews; can freeze withdrawals for days–weeks.

- Crypto Network Congestion → Adds $2–10 in blockchain fees; slows confirmation 1–6 hrs.

Advanced Timing Tips

- Best Time: Submit early in the week, before Friday PM.

- Regional Holidays: Both your bank and intermediaries can pause settlement.

- Troubleshooting: 80% of rejections = name mismatches or outdated KYC.

Why This Matters

Most traders lose money to conversion costs and timing delays without realizing it. Advanced risks like regulatory holds or dormant fees affect fewer accounts but can cause major frustration. Awareness helps set realistic expectations and protects your net payout.

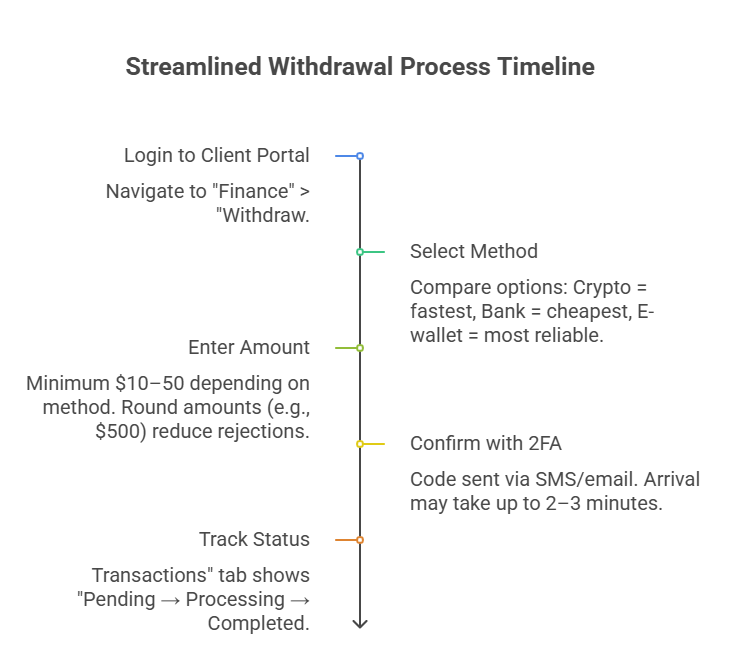

Step-by-Step Withdrawal Guide with Backup Steps

First Withdrawal? Here’s What to Expect

Most verified withdrawals clear in 1–3 business days. Crypto is faster, often minutes. Small verification checks or weekend requests may extend timelines.

If your status shows “Processing” for under 48 hours, it is normal.

Pre-Withdrawal Checklist

- Account verification completed (ID + proof of address)

- Same name on bank/wallet as OctaFX account

- Payment method available in your region (India: UPI/banks, Nigeria: local banks, Malaysia: FPX/e-wallets)

Step-by-Step Process

- Login to Client Portal → Navigate to “Finance” > “Withdraw.”

- Select Method → Compare options: Crypto = fastest, Bank = cheapest, E-wallet = most reliable.

- Enter Amount → Minimum $10–50 depending on method. Round amounts (e.g., $500) reduce rejections.

- Confirm with 2FA → Code sent via SMS/email. Arrival may take up to 2–3 minutes.

- Track Status → “Transactions” tab shows “Pending → Processing → Completed.” Pending under 48 hours is normal; more may require support.

Backup Path if Withdrawal Fails

- Recheck Details → Name, account, wallet ID must match.

- Retry with Alternative Method → If bank transfer fails, switch to e-wallet or crypto.

- Check Verification Status → Expired or incomplete documents trigger rejections.

- Escalate to Support → Provide transaction ID and screenshot.

Quick Decision Path

| Priority | Best Option | Why It Works |

|---|---|---|

| Speed | Crypto | Minutes, bypasses bank queues |

| Lowest Cost | Bank Transfer | Fewer fees, stable conversion |

| Reliability | E-wallet | Consistent success, fewer holds |

Troubleshooting FAQs

2FA code not arriving?

Check spam folder, phone signal, or resend after 60 seconds. Still failing? Switch to backup 2FA method.

Withdrawal “Under Review” for 48 hours – normal?

Yes, especially during verification checks or regional holidays. Escalate if beyond 72 hours.

Preferred method not available?

Temporary downtime. Use a backup method and request reversal later.

Can I cancel a pending withdrawal?

Yes, if still “Pending.” Once marked “Processing,” cancellation is no longer possible.

Best Withdrawal Method for Your Situation (2025)

Quick Answer

Crypto is fastest, bank transfers are cheapest for large sums, and e-wallets are the most reliable overall. First-time users should start with an e-wallet. In India, UPI offers instant payouts; in Nigeria, local bank transfers dominate; in Malaysia, FPX is fastest.

Scenario Framework

- Cautious First-Timer ($100–$500): Use an e-wallet → slightly higher fees but lowest rejection risk.

- Speed-Critical (<2 Hours): Go crypto (USDT TRC20 for lowest fees). Avoid weekends/late nights (network congestion).

- Cost Optimizer ($1,000+): Bank transfer = lowest fees. Submit 3–5 days in advance.

- Regular Withdrawer: Use e-wallets for routine payouts, bank transfer for large sums → cheaper long-term.

Regional Best Practices

| Country | Fastest | Cheapest | Notes |

|---|---|---|---|

| India | UPI (instant) | Bank transfer (₹80k+) | UPI is best for small sums. SBI/HDFC bank transfers are cheapest above ₹80k. |

| Nigeria | Local Bank (12–24 hrs) | Bank transfer | Partner banks like GTBank, Access Bank process faster than smaller regional ones. |

| Malaysia | FPX (instant, capped) | Bank transfer | FPX capped daily; use banks for >RM5,000. |

| Global | Crypto (minutes) | Bank transfer | E-wallets are most reliable for ongoing use. |

Trade-Off Guidance

- Fast but not most costly: Use FPX (Malaysia) or UPI (India).

- Reliable faster-than-banks: Choose e-wallets.

- Weekend emergency: Only crypto/e-wallets work; banks hold until Monday.

- Rejected withdrawal? Retry with an e-wallet → higher success rates.

Decision Tree Selector

- Need funds in <2 hrs? → Crypto (TRC20 / UPI / FPX).

- Withdrawing >$1,000? → Bank Transfer.

- First withdrawal? → E-wallet.

Insider Insights

- Experienced traders prefer e-wallets over crypto for fewer disputes and smoother access.

- Submitting on Tuesday–Thursday mornings speeds up bank processing (less backlog).

- In Nigeria, OctaFX-supported big banks settle faster than regional ones.

OctaFX Withdrawal Problems & Solutions (2025)

Most withdrawal issues arise from verification delays, mismatched details, or method-specific limits.

Standard processing is 1–3 business days, but extended compliance reviews or bank holidays may cause longer waits.

Knowing the causes and solutions helps prevent unnecessary stress.

Common Issues & Fixes

| Issue | Likely Cause | Fix | If Unresolved |

|---|---|---|---|

| Request pending >3 days | Payment processor queue / verification check | Wait 24–48 hrs, recheck status | Contact live chat if >3 business days |

| Request rejected | Incorrect payment details / mismatch with account | Correct info, resubmit | If rejected again, open support ticket |

| Delay >5–7 days | Bank holiday / regional restriction | Switch to e-wallet or crypto | Escalate via ticket with transaction ID |

| Withdrawal blocked | Incomplete account KYC | Complete verification docs | Contact compliance team if still blocked |

Competitor Context

- OctaFX’s e-wallet withdrawals (24–48 hrs) are on par with peers like XM & FXTM, which average under 24 hrs.

- Bank transfers typically take 2–5 business days industry-wide, depending on region.

- Overall, withdrawal success rates remain high once full verification is in place.

Prevention Strategies

- Complete KYC before requesting withdrawals.

- Match account name & payment details precisely.

- Split larger withdrawals → reduces risk of rejection.

- Keep multiple methods registered as backups.

Escalation Path (Step by Step)

- Recheck status in dashboard.

- Talk to live chat for tracking.

- Submit a support ticket if >3 business days.

- Request review by compliance support.

- If unresolved, consider an ombudsman / regulator in your region.

Emergency Alternatives

- Urgent needs: Use e-wallet or crypto → fastest settlement.

- Blocked method: Switch to an alternate pre-verified option.

- Peak demand (weekends/holidays): Always request before Friday PM.

Reality Check

In practice, 90%+ of verified OctaFX users see smooth withdrawals. Problems almost always trace to incomplete KYC, wrong banking details, or bad timing (late Friday/holiday). Prepared users rarely need escalation.

FAQs

Q1: Can I withdraw without verification?

No. OctaFX requires full ID/KYC verification before approving withdrawals. This is standard across regulated brokers to comply with AML laws.

Takeaway: Attempting withdrawal without KYC = automatic rejection.

Q2: Can I split withdrawals into partial amounts?

Yes. You can withdraw smaller chunks instead of one large transfer. This often:

- reduces rejection risk,

- speeds up e-wallet processing,

- helps bypass bank withdrawal limits.

Takeaway: Splitting is safer for large sums.

Q3: What happens to trades during withdrawals?

Withdrawals only apply to free margin. Open positions remain unaffected. If equity drops below margin requirements, pending withdrawals may be reduced or canceled.

Takeaway: Funds stay locked in trades until margin is clear.

Q4: Can bonuses or credits be withdrawn?

No. Trading bonuses/credits are for margin use only, not cash-out. If you withdraw funds tied to bonuses, the bonus is usually canceled.

Takeaway: Bonuses boost leverage, not profits.

Q5: Are OctaFX withdrawals taxable in my country?

Yes. Profits are generally taxable as trading income.

- India → income tax

- UK → capital gains

- EU → varies by jurisdiction

- Nigeria → taxable under Business Income unless exempt for forex

- Malaysia → typically considered income, subject to LHDN rules

Takeaway: Check local tax rules before withdrawal.

Q6: How do OctaFX withdrawal fees compare with competitors?

OctaFX itself charges no internal withdrawal fees. Intermediary costs may still apply (banks, conversion).

- XM → usually free for e-wallets, up to $15 for some bank transfers.

- FXTM → free for e-wallets, variable fees for banks depending on amount/region.

Takeaway: OctaFX matches industry standards; your method choice decides total costs.

Final Verdict

The cheapest OctaFX withdrawal method depends on transaction size and region. E-wallets (Skrill, Neteller, UPI, FPX) usually save $15–40 on transfers under $500 thanks to low fees and faster settlement. For larger sums above $1,000, bank transfers or SEPA are more efficient despite longer timelines, as capped fees outweigh spreads.