Arbitrage in trading is the practice of simultaneously buying and selling the same asset across different markets to profit from price differences. It relies on market inefficiencies and aims to generate risk-free gains without betting on price direction.

While strategies like spatial, triangular, and statistical arbitrage offer short-term opportunities, real-world execution involves challenges. Slippage, latency, liquidity gaps, and transaction fees often erode profits.

Arbitrage appears risk-free in theory, it demands fast execution, capital allocation, and automation, making it less accessible and far more complex than it seems.

Markets Where Arbitrage Occurs (Forex, Crypto, Stocks, Commodities)

Arbitrage opportunities exist across all major asset classes where the same instrument or equivalent exposure is available in more than one market or exchange:

- Forex Markets

- Cryptocurrency Markets

- Stock Markets

- Commodities

How Arbitrage Works (With Simple Example)

Buy Low, Sell High Logic

Arbitrage operates on a risk-controlled principle: identify a price discrepancy for the same asset across two or more markets, then simultaneously buy in the cheaper market and sell in the more expensive one.

The trades are executed without speculating on the asset’s future price, profit is captured immediately from the pricing gap itself.

Execution must be near-instant to prevent price convergence from erasing the opportunity. Arbitrage assumes market neutrality, meaning that the trader is not exposed to directional price movement, only the differential between markets matters.

The gross profit from arbitrage is calculated as:

Profit = Sell Price – Buy Price – Transaction Costs – Slippage – Fees

Real Example – BTC Price on Binance vs Coinbase

Assume the following market conditions:

- BTC/USDT on Binance is trading at $29,850

- BTC/USDT on Coinbase is trading at $30,000

A trader identifies the $150 price gap and executes the following:

- Buys 1 BTC on Binance at $29,850

- Simultaneously sells 1 BTC on Coinbase at $30,000

If both trades are executed without slippage and the combined fees are under $150, the trader captures the difference as profit. Assuming fees total $40:

Net Arbitrage Profit = $30,000 – $29,850 – $40 = $110

This profit is “locked in” immediately—there is no need to predict where BTC will move next.

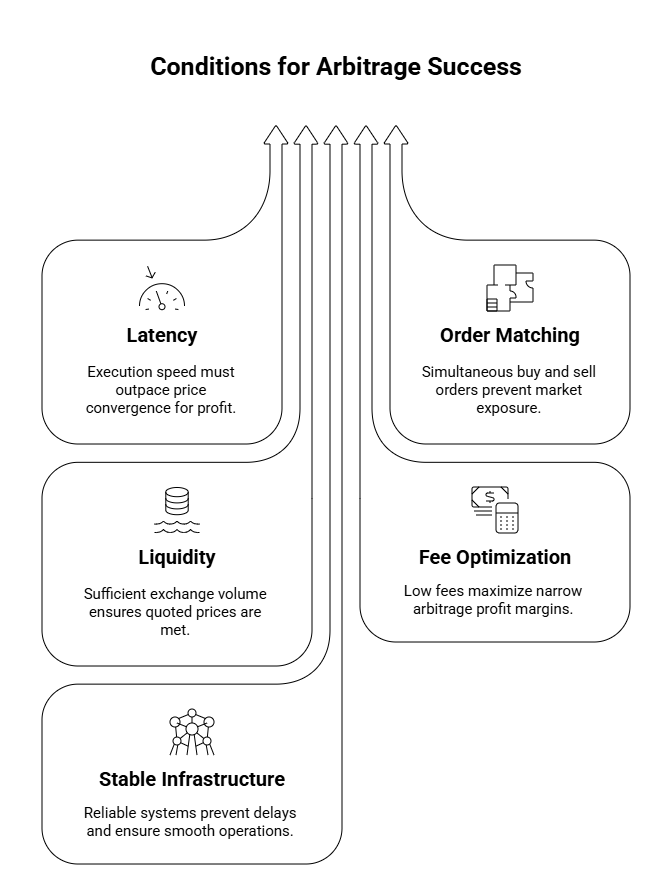

Conditions for Successful Arbitrage Execution

To capitalize on arbitrage opportunities, several technical and operational conditions must be met:

- Latency: Execution speed must be faster than price convergence. Manual trades rarely suffice.

- Order Matching: Both legs (buy and sell) must fill simultaneously to prevent exposure.

- Liquidity: Both exchanges must support sufficient volume at quoted prices.

- Fee Optimization: Arbitrage margins are narrow; high taker fees or withdrawal fees can nullify profits.

- Stable API or Trading Infrastructure: Bots or systems must operate without delay, error, or downtime.

Even minor delays, slippage, or liquidity gaps can turn a profitable spread into a net loss.

Types of Arbitrage Strategies

Arbitrage strategies vary based on asset class, market structure, and execution method. While the core principle remains the same, profiting from price discrepancies, each type has unique logic, risk characteristics, and infrastructure requirements.

Below are the most common and relevant types of arbitrage strategies across forex, crypto, and traditional markets.

Spatial/Geographical Arbitrage

This strategy exploits price differences for the same asset across different exchanges or regions. It is the most basic form of arbitrage and requires traders to monitor real-time price feeds across multiple platforms.

- Example: ETH/USDT trades at $2,500 on Kraken and $2,530 on Binance. Buying on Kraken and selling on Binance captures a $30 spread per unit.

- Requirements: Multi-exchange access, API automation, rapid execution, and fee management. Withdrawals and transfer times can impact execution viability.

- Common In: Crypto, forex, commodities, stocks listed in multiple markets.

Triangular Arbitrage

Triangular arbitrage takes advantage of pricing inefficiencies between three currency pairs in the same market. It is commonly used in forex and crypto markets with high liquidity.

- Example:

- Convert USD to EUR

- Convert EUR to GBP

- Convert GBP back to USD

If the final USD amount is greater than the initial, a profitable loop exists.

- Convert USD to EUR

- Requirements: Real-time multi-leg execution, ultra-low latency, precise exchange rate calculations.

- Common In: Forex brokers, crypto exchanges with active cross-pair listings.

Statistical Arbitrage

Statistical arbitrage (or “stat arb”) uses quantitative models to identify mean-reverting relationships between correlated assets. Trades are placed based on statistical probabilities rather than clear price gaps.

- Example: If two historically correlated stocks diverge temporarily, a trader may go long on the undervalued stock and short the overvalued one, expecting them to revert.

- Requirements: Advanced data analysis, algorithmic execution, historical data, and model calibration.

- Common In: Equities, ETFs, crypto pairs with strong historical correlation.

Risk Arbitrage (Merger Arbitrage)

This strategy involves buying and selling stocks of companies involved in mergers or acquisitions. The trader anticipates that the target company’s stock will converge toward the announced acquisition price.

- Example: Company A announces it will acquire Company B for $50/share. Company B’s current price is $47. The arbitrageur buys at $47, expecting to gain $3 once the deal finalizes.

- Risks: Regulatory failure, deal collapse, delays. Not entirely risk-free.

- Common In: Equity markets, particularly U.S. and European stock exchanges.

Crypto Arbitrage (CEX vs DEX)

Crypto arbitrage targets price discrepancies between centralized exchanges (CEXs) and decentralized exchanges (DEXs), or between regional markets.

- Example: A token trades at $1.02 on Uniswap and $1.08 on Binance. Buy from Uniswap and sell on Binance.

- Variations: DEX-to-DEX arbitrage, CEX-to-CEX, or cross-chain arbitrage using bridges.

- Challenges: Gas fees, slippage, front-running, failed transactions, and network congestion.

- Common In: DeFi ecosystems (Ethereum, BNB Chain, Solana), volatile token pairs.

Why Arbitrage Is Considered “Risk-Free” (But Isn’t Always)

Arbitrage is often referred to as a “risk-free” trading strategy because, in theory, it involves no market exposure, profits are made purely from temporary price differences across markets.

However, in practice, arbitrage execution carries multiple layers of operational and financial risk that can turn expected profits into losses.

Below is a breakdown of the theoretical appeal and real-world limitations.

Theoretical Assumption vs Practical Execution

In theory, arbitrage assumes:

- Immediate execution of both buy and sell orders

- No price slippage between order placement and fill

- No transaction or withdrawal fees affecting net profit

- Infinite liquidity on both sides

- Perfect market access without delay

In reality:

- Price gaps can vanish before both legs execute

- Orders may partially fill or fail entirely

- Fees, spreads, and network costs can exceed expected profit

- Latency between exchanges causes mismatches

- Liquidity imbalances lead to failed or delayed settlement

Thus, while arbitrage can be market-neutral, it is not operationally risk-free.

Execution Risks – Latency, Slippage, and Fees

Execution risk is the primary reason arbitrage fails to remain “risk-free”:

- Latency: Delays in price feed updates or order transmission can cause missed or mispriced trades.

- Slippage: Prices change between the time you identify an opportunity and execute the trade.

- Taker/Maker Fees: These fees can reduce or eliminate your arbitrage spread, especially in low-margin trades.

- Withdrawal/Transfer Fees: In crypto, withdrawing tokens across chains or between exchanges can be costly and time-consuming.

- API Errors: Failures in trading bots or connection issues can result in unhedged or one-sided execution.

Capital Lock, Market Timing, and Liquidity Limits

Even when arbitrage appears possible, real-world conditions may prevent execution:

- Capital Requirements: Effective arbitrage demands sizable capital across multiple platforms to absorb spreads and fees.

- Transfer Delays: Funds may be stuck in transit or under withdrawal hold, preventing rebalancing.

- Market Depth: Lack of order book depth can prevent full execution at expected prices.

- Timing Risks: Even short-term changes in volatility or spread compression can close the arbitrage window prematurely.

- Regulatory Friction: Capital controls or compliance checks can delay arbitrage in cross-border environments.

Tools and Platforms Used for Arbitrage

Arbitrage trading requires fast execution, synchronized market access, and reliable infrastructure.

The following tools form the foundation for both manual and automated arbitrage setups across forex, crypto, and equities.

Algorithmic Bots

Arbitrage bots are automated systems designed to detect and execute arbitrage opportunities within milliseconds. These bots continuously monitor multiple markets for price discrepancies and execute trades once the profit exceeds a predefined threshold, factoring in slippage and fees.

- Functions: Monitor bid/ask spreads, execute multi-leg trades, handle order routing

- Advantages: Instant execution, 24/7 operation, emotionless decision-making

- Limitations: Require technical setup, exchange API integration, and maintenance

- Popular Use Cases: CEX-CEX crypto arbitrage, triangular forex arbitrage

- Examples: Hummingbot, Gimmer, Bitsgap (crypto); MetaTrader scripts (forex)

Arbitrage Scanners

Scanners are analytical tools that identify real-time price differences across exchanges or markets. Unlike bots, scanners do not execute trades but provide actionable intelligence to the trader.

- Functions: Compare asset prices across platforms, rank arbitrage potential

- Features: Custom spread filters, real-time alerts, exchange support lists

- Use Cases: Manual arbitrage, strategy testing, opportunity validation

- Examples: CoinMarketCap Arbitrage, Cryptohopper Scanner, Arbitrage.Expert

- Limitation: Manual execution still requires latency-aware action

Broker/API Access & Exchange Speed

Fast, reliable broker or exchange connectivity is critical to arbitrage execution. Traders must operate through platforms offering low-latency APIs, minimal downtime, and high order execution reliability.

- Key Factors:

- REST or WebSocket API access with stable endpoints

- Proximity hosting or co-location (for institutional scale)

- Taker/maker fee structure clarity

- Asset pair depth and refresh rate

- REST or WebSocket API access with stable endpoints

- Forex & Stock: Use brokers like Interactive Brokers, Pepperstone, Saxo Bank

- Crypto: Binance API, Kraken, Bybit, KuCoin—all offer open, rate-limited APIs

Latency differences, even in milliseconds, can render arbitrage non-viable.

Real-World Examples of Arbitrage in Action

Arbitrage becomes tangible when applied to real trading conditions across different markets.

Below are actual use cases that demonstrate how pricing inefficiencies appear, and how traders attempt to capitalize on them.

Crypto Exchange Gaps

Crypto markets often exhibit price discrepancies due to fragmentation across centralized and decentralized exchanges. This is especially common during periods of high volatility or news-driven volume spikes.

- Example:

- BTC/USDT trades at $30,150 on Binance

- The same pair trades at $30,350 on Kraken

- A trader buys on Binance and sells on Kraken, capturing a $200 price gap

- After accounting for taker fees, withdrawal fees, and slippage, net profit is retained if spread > total cost

- BTC/USDT trades at $30,150 on Binance

- Key Insight: Latency, transfer delays, and withdrawal limits can erode real returns, especially in cross-exchange arbitrage.

Forex Triangular Conversion Loops

Triangular arbitrage arises when three currency exchange rates create a closed-loop discrepancy, allowing traders to profit from relative mispricing.

- Example:

- Convert USD → EUR at 0.90

- Convert EUR → GBP at 0.88

- Convert GBP → USD at 1.30

- Theoretically, $1 → €0.90 → £0.792 → $1.0296

- This creates a 2.96% arbitrage opportunity (before transaction costs)

- Convert USD → EUR at 0.90

- Key Insight: Requires near-zero latency and very high liquidity across pairs. Commonly executed by HFT firms.

Stock Dual Listings Arbitrage

Some multinational companies are listed on multiple stock exchanges, and price discrepancies arise due to currency shifts, market hours, or liquidity.

- Example:

- Royal Dutch Shell (RDSA) trades on both the London Stock Exchange and Euronext Amsterdam

- If the GBP-euro adjusted price diverges beyond the fee threshold, traders arbitrage the gap

- Institutional desks typically use this method with algorithmic trade balancing

- Royal Dutch Shell (RDSA) trades on both the London Stock Exchange and Euronext Amsterdam

- Key Insight: Requires FX conversion logic and synchronized access to both exchanges. Often used by quant funds and arbitrage desks.

Commodity Arbitrage (Gold, Oil, etc.)

Arbitrage in commodities occurs when the price of a raw material diverges between regional exchanges or between spot and futures markets.

- Example:

- Gold trades at $1,960/oz on COMEX (US)

- Simultaneously trades at $1,975/oz on MCX (India, adjusted for currency and tax)

- Traders with access to both markets attempt to exploit the spread

- Gold trades at $1,960/oz on COMEX (US)

- Key Insight: Requires factoring in logistics, taxes, import/export rules, and exchange rate conversion. Typically not accessible to small retail traders.

Bottom Line

Arbitrage is a market-neutral trading strategy that exploits temporary price differences across exchanges or instruments to generate low-risk profit. While it appears “risk-free” in theory, real-world execution introduces latency, slippage, liquidity constraints, and infrastructure costs that make consistent profitability challenging, especially for retail traders.

Success in arbitrage depends on automation, multi-market access, precise execution, and capital efficiency.

For beginners, arbitrage offers a gateway to understanding how markets self-correct and where inefficiencies arise, but it should be approached with realistic expectations, technical readiness, and a focus on execution risk over theoretical appeal.

FAQs

Q1. Can anyone do arbitrage trading?

Technically yes, but consistently profitable arbitrage requires access to fast execution tools, multiple market accounts, and sufficient capital. Retail traders can attempt simple forms like CEX-to-CEX crypto arbitrage, but institutional players dominate high-frequency and cross-market arbitrage due to superior infrastructure.

Q2. Is arbitrage legal?

Yes, arbitrage is legal in all major financial markets. It plays a key role in improving market efficiency by aligning prices across platforms. However, traders must follow regulations related to exchange use, tax reporting, and cross-border fund movement. Front-running or manipulation under the guise of arbitrage is illegal.

Q3. Can arbitrage be done manually?

Manual arbitrage is possible but rarely efficient. By the time a retail trader spots a price difference and attempts execution, the spread often closes. Manual execution may work in illiquid altcoin markets or during temporary exchange lags, but most viable arbitrage now depends on automation and bots.

Q4. Why isn’t arbitrage common among retail traders?

Retail traders face several barriers:

- Higher relative transaction fees

- Slow execution and lack of automation

- Capital fragmentation across platforms

- Withdrawal delays and compliance restrictions

- Limited access to institutional-grade tools and APIs

These factors reduce the feasibility of consistent arbitrage profits at retail scale.

Q5. Are there arbitrage opportunities in crypto?

Yes, crypto offers the highest frequency of arbitrage opportunities due to exchange fragmentation, price volatility, and varying liquidity across platforms. Traders exploit CEX-CEX, CEX-DEX, and DEX-DEX spreads. However, high gas fees, slippage, front-running, and failed transactions make execution more complex than it appears.

Sharpen your skills, check out our blog for trading tips.