Algorithmic trading works by using pre-defined rules to automatically execute trades based on market conditions.

A strategy is coded or set through a platform, which then monitors live market data. When the specified conditions are met, such as a moving average crossover, the system sends orders directly to the exchange through broker APIs.

This process eliminates manual intervention, ensures faster execution, and operates with strict logic across multiple instruments in real time.

What Is Algo Trading? (With Real-World Example)

Algorithmic trading is the use of computer programs to automatically place buy or sell orders based on pre-defined logic. Traders encode rules, such as price, volume, or indicators, that the system executes when conditions are met.

Manual vs Algorithmic Execution

- Manual Trading: The trader monitors the market and places each trade based on discretion or analysis.

- Algo Trading: A set of conditions is predefined. The system monitors the market, and trades are executed automatically once those rules are met—without manual input.

Example: Buy When 20EMA > 50EMA

Suppose the strategy is to buy a stock when the 20-period Exponential Moving Average (EMA) crosses above the 50-period EMA.

The algo constantly checks for this crossover. Once it occurs, the order is placed automatically, without waiting for human action.

Where Is Algo Trading Used?

- India: Widely used on NSE and BSE through broker APIs.

- US: Common on NYSE and NASDAQ, integrated with institutional desks.

- Crypto: Active on platforms like Binance for 24×7 automated trading.

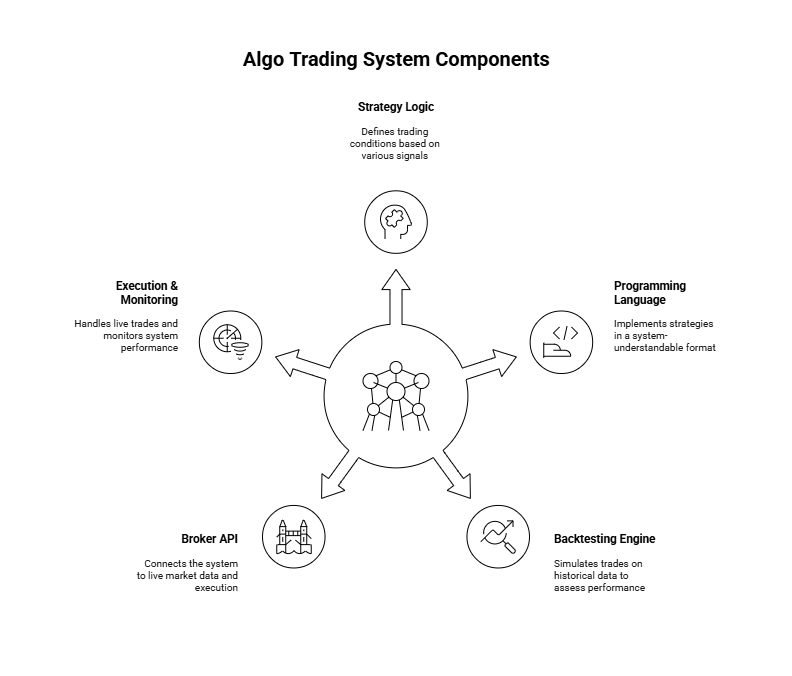

Core Components of an Algo Trading System

Algorithmic trading relies on five key components that enable fully automated execution without human input.

1. Strategy Logic (Rule Engine)

This defines the conditions under which trades are executed. The logic can be based on price movements, indicators, or quantitative signals.

Common strategy types:

- Trend Following

- Mean Reversion

- Arbitrage

- Options-Based Models

- High-Frequency Trading (HFT)

2. Programming Language or No-Code Builder

The strategy must be implemented in a way the system understands.

- For developers: Python, MQL4/5, Pine Script (used in MetaTrader, TradingView).

- For non-coders: Platforms like Streak, Tradetron, and AlgoTest offer drag-and-drop interfaces to build rule-based systems.

3. Backtesting Engine

Before deploying a strategy, the system must simulate trades on historical data to assess performance.

Key metrics:

- Sharpe Ratio

- Win Rate

- Maximum Drawdown

- Profit Factor

- Expectancy

4. Broker API & Exchange Gateway

This is the connection layer between the trading system and the live market. Broker APIs provide access to:

- Market price feeds (real-time data)

- Order execution

- Account and margin data

- Position tracking

- Exchange-level compliance (e.g., NSE, BSE, NYSE)

5. Execution & Monitoring System

Once deployed, the system handles live trade execution and monitors for:

- Order slippage

- System uptime

- Risk parameters (e.g., max loss per day)

- Alerts for exceptions

- Continuous compliance and position tracking

How Algo Trading Works: Step-by-Step Process

Algo trading operates through a structured pipeline that transforms a trading idea into an automated, live-executing system.

The process involves five clearly defined stages:

- Strategy Design

- Backtesting

- Paper Trading

- Live Deployment

- Execution & Monitoring

Algo Trading Process: Step-by-Step Overview

| Step | Stage | Action Performed | Tools Involved |

| 1 | Strategy Design | Define logic-based rules (e.g., Buy when EMA20 > EMA50) | TradingView, Excel, Pinescript, Python |

| 2 | Backtesting | Apply strategy to historical data and analyze performance metrics | AlgoTest, QuantConnect, MetaTrader |

| 3 | Paper Trading | Run strategy on live market data without real money to test execution behavior | TradingView Paper Account, Streak |

| 4 | Live Deployment | Connect algo to broker API and push strategy for real-time trading | Zerodha Kite Connect, Broker APIs |

| 5 | Execution & Monitoring | Monitor trades, system logs, price feeds, and enforce real-time risk controls | Tradetron, Broker Terminals, Custom UI |

Each step serves a distinct function, ensuring that the logic is sound, the performance is tested, and the automation is safely deployed in real market environments.

Below is a detailed breakdown of each stage.

Step 1: Strategy Design

Purpose: Define the rules and logic under which the system will operate.

The first step involves specifying the exact conditions that trigger a trade. This includes defining entry and exit points based on technical indicators, price action, volume, or statistical models.

For example:

- Entry Rule: Buy when the 20-period EMA crosses above the 50-period EMA.

- Exit Rule: Sell when the RSI exceeds 70 or the EMA crossover reverses.

The rules must be:

- Objective (not based on human discretion)

- Backtestable (quantifiable on historical data)

- Precise (no ambiguous or overlapping conditions)

This stage also includes setting risk parameters:

- Stop-loss level

- Take-profit target

- Maximum number of trades per day

- Capital allocation per trade

The strategy can be created via:

- Code-based logic (Python, Pine Script, MQL4/5)

- No-code platforms (Streak, Tradetron, AlgoTest)

Output: A clearly defined trading algorithm that can be programmed or configured in a system.

Step 2: Backtesting

Purpose: Validate the logic using historical market data.

Backtesting simulates how the strategy would have performed in the past using actual price data. This helps assess viability before risking real capital.

What is tested:

- Profitability across different timeframes

- Consistency in trending and sideways markets

- Frequency of trades

- Risk-adjusted return

Key performance metrics:

- Sharpe Ratio – risk-adjusted returns

- Win Rate – percentage of profitable trades

- Maximum Drawdown – largest loss from peak to trough

- Expectancy – average profit per trade over time

- Profit Factor – ratio of gross profit to gross loss

Good backtesting practices:

- Use high-quality, granular data (tick or minute-level)

- Avoid lookahead bias (using future data in past logic)

- Include realistic assumptions (slippage, commissions)

Output: Statistical report confirming whether the logic is viable under historical market conditions.

Step 3: Paper Trading

Purpose: Test the algorithm in live market conditions without risking capital.

Paper trading places virtual orders in real time using the same strategy logic and market feed. This simulates how the algorithm would behave in live conditions, helping to identify:

- Latency issues (delays in execution)

- API failures or disconnections

- Overtrading or false triggers due to noisy data

- Logical bugs not caught in backtesting

- Incompatibility with exchange-level rules (e.g., order throttling, margin limits)

Paper trading bridges the gap between theoretical performance and real-time behavior. Unlike backtesting, which assumes ideal execution, paper trading reveals practical challenges.

Most algo platforms (like TradingView, Streak, or broker terminals) offer built-in paper trading environments. Some APIs also support sandbox mode.

Output: Confirmation that the algorithm behaves as expected under live conditions.

Step 4: Live Deployment

Purpose: Connect the strategy to a broker for live trading.

Once validated, the strategy is deployed by linking the system to a broker or exchange using Broker APIs. These APIs enable:

- Real-time market data streaming

- Automated order routing

- Position tracking and order status updates

- Access to account details (margin, P&L, exposure)

For Indian markets, common broker APIs include:

- Zerodha Kite Connect

- Upstox API

- Angel One SmartAPI

- FYERS API

Live deployment also requires:

- API key/secret setup

- Access token refresh system (automated or manual)

- Mapping of strategy logic to exchange symbols and order types

Security is critical. Deployment often involves setting:

- Firewalls and IP whitelisting

- Fail-safes for internet/power outages

- Authentication for order confirmation

Output: The algo is now connected and ready to place real trades.

Step 5: Execution & Monitoring

Purpose: Automatically place and track trades based on live data.

The final stage is real-time execution. The system continuously monitors live market feeds and triggers buy/sell orders once the conditions are met.

Tasks handled at this stage:

- Auto-order placement with real-time price

- Execution checks (limit vs market order, partial fills)

- Trade logging and audit trails

- Risk monitoring (e.g., stop-loss triggered, max drawdown reached)

- Alerts and notifications (email, SMS, webhook, etc.)

Monitoring systems ensure:

- Latency stays within acceptable limits

- Orders don’t loop due to logic errors

- Exposure and margin usage are within defined limits

- Errors (e.g., broker downtime, data feed issues) are caught and handled immediately

If anomalies occur, trades can be paused, adjusted, or terminated depending on predefined rules.

Some platforms also support:

- Live dashboards

- Kill-switch functionality

- Portfolio-wide performance tracking

Output: The system runs continuously, executing trades without manual intervention, under constant supervision.

Benefits and Risks of Algo Trading

Algorithmic trading offers operational advantages that improve efficiency, consistency, and scalability. However, it also introduces specific technical and regulatory risks that must be managed.

Key Benefits

1. Emotion-Free Execution

Trades are executed based solely on pre-defined logic, eliminating human emotions such as fear, greed, or hesitation. This ensures consistency and discipline, especially in volatile markets.

2. Faster Order Placement

Algo systems respond to market signals in milliseconds. The reduced reaction time enables traders to capture opportunities that are often missed during manual execution.

3. 24×7 Market Monitoring

Automated systems continuously monitor price feeds and market data, ensuring no opportunity is missed, even during off-hours in global or crypto markets.

4. Backtestable Logic

Strategies can be tested on historical data before going live. This allows traders to analyze risk-return ratios, validate assumptions, and optimize performance based on quantifiable metrics.

5. Scalability Across Instruments

A single algorithm can manage multiple assets simultaneously, enabling diversification across stocks, options, currencies, or crypto—without increasing operational workload.

Key Risks

1. Overfitting During Backtest

An overly optimized strategy may perform well in historical data but fail in live markets. Overfitting leads to unreliable results and false confidence in system accuracy.

2. System Failures and API Errors

Hardware issues, unstable internet, broker-side disruptions, or API authentication failures can interrupt trade execution or cause missed signals.

3. Slippage in Volatile Markets

In fast-moving markets, the executed price may differ from the intended price. This slippage reduces profitability and increases execution risk, especially in low-liquidity environments.

4. Regulatory Constraints (India-Specific)

In markets like India, APIs have strict regulatory limits on order rates, strategy approvals, and algo certification. Breaching compliance may result in penalties or order rejections.

5. Lack of Manual Supervision

If left unmonitored, a faulty strategy or coding error can lead to uncontrolled trades, unintended losses, or margin breaches. Manual oversight is essential for risk containment.

FAQs:

Q1. How does an algo know when to buy or sell?

The algorithm follows a set of predefined rules coded into the system. These rules are based on indicators, price levels, or statistical triggers. When the conditions are met, for example, “buy when EMA20 crosses above EMA50”, the system executes the trade automatically.

Q2. What kind of data does it use?

Algo systems use live and historical market data, including:

Price (OHLC):

- Volume

- Technical indicators (e.g., RSI, MACD)

- Order book depth

- Volatility and momentum metrics

This data is sourced through broker APIs or exchange feeds.

Q3. How does it connect to the stock exchange?

Algo platforms connect to stock exchanges (like NSE or NYSE) through authorized broker APIs. These APIs allow the system to receive real-time data, place orders, manage positions, and receive trade confirmations.

Q4. Can I build my own strategy without coding?

Yes. Platforms such as Streak, Tradetron, and AlgoTest offer no-code strategy builders. These allow users to define entry/exit rules using dropdowns and logic blocks—no programming required.

Q5. Do I need to learn programming?

Not necessarily. If you want to build highly customized strategies, coding (e.g., in Python or Pine Script) provides more flexibility. However, many retail-friendly platforms now offer no-code interfaces to simplify access.

Q6. Can I trade using algo on NSE/BSE?

Yes. Several brokers in India support API-based algo trading on NSE and BSE, including Zerodha, Upstox, Angel One, and FYERS. You may need to comply with exchange-level guidelines for order frequency and strategy certification.

Q7. Is algo trading safe for beginners?

Algo trading is efficient but not risk-free. Beginners should start with backtesting and paper trading before deploying live strategies. Platform reliability, risk management, and manual oversight are essential for safe execution.

Learn the latest trading tricks from our official blog.