Margin is the upfront capital, set as a percentage of the contract value, required to initiate a commodity futures trade.

Leverage allows traders to control a larger position with a smaller margin, amplifying both gains and losses.

For example, a 10% margin creates 10x leverage. Daily mark-to-market (MTM) adjusts this margin based on price movements.

Exchanges like MCX and CME define minimum margin and leverage limits, while brokers may impose stricter controls. Falling below the maintenance margin triggers a margin call.

If not replenished, positions are squared off. Understanding these mechanics is essential for managing risk effectively.

What Is Margin and How Do You Calculate It (With Examples)

Margin vs. Full Contract Value

Margin is the capital required to enter a commodity futures position, expressed as a percentage of the total contract value. It acts as collateral to cover potential daily losses.

The full contract value represents the notional worth of the underlying asset and is the basis on which the margin is computed.

Understanding their relationship is critical for evaluating leverage, exposure, and funding requirements.

Margin vs. Full Contract Value , Side-by-Side Breakdown

| Aspect | Full Contract Value | Margin |

| Exposure | 100% of underlying asset | 5% to 15% of contract value |

| Purpose | Reflects total transaction worth | Capital required to initiate position |

| Risk Coverage | None | Used as collateral for MTM loss |

| Volatility Impact | Full price swings absorbed | Controlled via SPAN + Exposure |

Formula: Margin = Contract Value × Margin %

The margin is derived by multiplying the contract value by the applicable margin percentage. This percentage is assigned by the exchange based on price volatility, liquidity risk, and instrument classification. This formula enables traders to assess capital needs for any commodity futures instrument.

How to Calculate Margin , Step-by-Step

- Identify lot size and current market price of the commodity

- Compute contract value = Lot Size × Price

- Apply margin percentage = Contract Value × Margin %

- Check SPAN and Exposure to compute total payable margin

Examples: Commodity Margin Calculations (MCX Crude Oil and Gold Mini)

Practical margin calculations illustrate how the margin requirement varies across instruments based on lot size, price, and exchange-defined margin percentage.

Example 1: MCX Crude Oil Futures

| Metric | Value |

| Lot Size | 100 barrels |

| Price | ₹6,500 per barrel |

| Contract Value | ₹6,50,000 |

| Margin % | 10% |

| Required Margin | ₹65,000 |

| SPAN / Exposure | ₹60,000 / ₹5,000 |

Example 2: MCX Gold Mini Futures

| Metric | Value |

| Lot Size | 100 grams |

| Price | ₹72,000 per 10 grams |

| Contract Value | ₹7,20,000 |

| Margin % | 11% |

| Required Margin | ₹79,200 |

| SPAN / Exposure | ₹70,000 / ₹9,200 |

SPAN Margin vs. Exposure Margin (Explained Simply)

SPAN (Standard Portfolio Analysis of Risk) margin is the core margin calculated through a risk-based model that accounts for price fluctuations and historical volatility. Exposure margin is a fixed additional requirement imposed to safeguard against extreme intraday volatility. Combined, these form the total margin requirement. Understanding their roles is crucial, as both are independently enforced by commodity exchanges to stabilize the market.

Initial vs. Maintenance Margin

Initial margin is the upfront capital required to open a futures position.

Maintenance margin is the minimum balance that must be maintained in the account to keep that position active.

If the margin balance drops below this level due to losses, a margin call is triggered. These thresholds are predefined by exchanges and modeled to ensure sufficient capital coverage.

Real examples of price drops breaching maintenance levels illustrate the risk buffer they create.

Why Daily MTM Affects Margin Balance

Mark-to-market (MTM) adjustment reflects the daily change in the contract’s market value, with gains added and losses deducted from the margin account. This impacts the usable margin and may reduce the margin below the maintenance threshold, triggering a top-up requirement. Understanding MTM is essential for managing daily risk and avoiding forced liquidation due to insufficient funds.

Understanding Leverage in Commodity Trading

Leverage amplifies exposure in commodity trading, how it is calculated, and who sets or limits it. Traders searching for this topic seek applied clarity, not generic knowledge. EEAT alignment here requires real examples, specific ratios, and exchange-specific context (MCX, CME).

How to Understand and Calculate Leverage (With Real Examples)

Leverage in commodity trading allows traders to control large contract values with a relatively small upfront margin. It increases market exposure and potential returns, but also amplifies risk.

Below is the mathematical structure of leverage, how to compute it from exchange requirements, and how it plays out in practical trades.

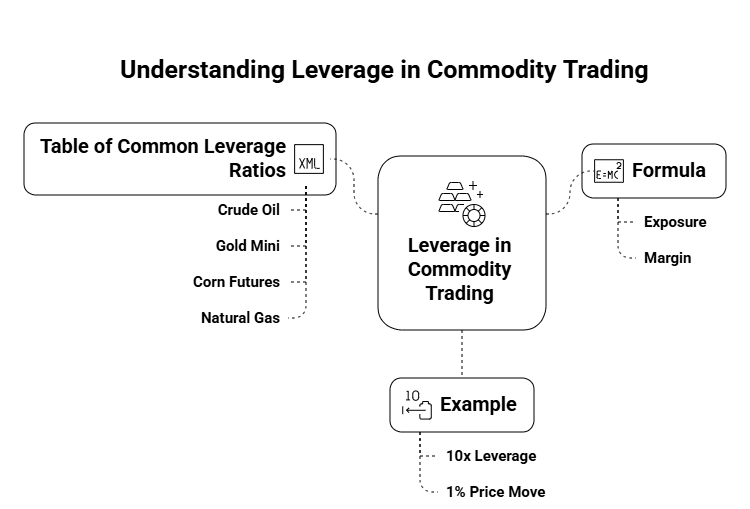

Formula: Leverage = Exposure ÷ Margin

Leverage is calculated by dividing the total exposure (i.e., contract value) by the margin amount deposited. This formula represents how many times a trader’s capital is multiplied in terms of market exposure. A higher ratio indicates greater exposure per unit of margin, and understanding this helps in evaluating capital risk and return potential.

Example: ₹1L Margin = ₹10L Exposure (10x Leverage)

A trader deposits ₹1,00,000 as margin to take a futures position with a notional value of ₹10,00,000. This creates a 10x leverage scenario. If the price moves 1% in the trader’s favor, it yields a 10% return on the margin. Conversely, a 1% adverse move causes a 10% capital loss. This example illustrates how small market changes result in magnified outcomes.

Table of Common Leverage Ratios (MCX, CME)

Leverage ratios vary by asset class and exchange rules. This table provides a reference for common leverage multiples available across commodities and exchanges. It helps traders benchmark instrument-specific leverage for metals, energy, and agri-commodities.

| Commodity | Exchange | Contract Value | Margin % | Leverage |

| Crude Oil | MCX | ₹10,00,000 | 10% | 10x |

| Gold Mini | MCX | ₹7,20,000 | 11% | 9.1x |

| Corn Futures | CME | $18,000 | 6% | 16.6x |

| Natural Gas | CME | $75,000 | 8% | 12.5x |

Who Controls Leverage: Broker vs Exchange Rules

Leverage isn’t universally fixed. While exchanges define maximum leverage via margin mandates (SPAN, Exposure), brokers may impose tighter limits based on client profile, volatility, or risk controls.

The below section identifies who controls leverage and how actual usable leverage can differ from headline limits.

When Brokers Offer Less Than Exchange Limits

Brokers can reduce leverage below exchange-defined maximums by increasing margin requirements. For example, an exchange may allow 10x leverage, but a broker may enforce only 5x for new or retail traders.

These restrictions protect both trader capital and broker exposure, especially during high volatility or low liquidity periods.

Tracking Available Leverage (SPAN Tools, Platforms)

Real-time leverage availability can be tracked using broker platforms, exchange SPAN margin calculators, or trading terminals. These tools reflect margin changes due to price fluctuation, volatility spikes, or policy revisions. Traders must monitor SPAN + Exposure adjustments to know their actual leverage capacity per contract.

Margin and Leverage Rules Across MCX, CME, and Other Exchanges

This section compares how major global exchanges , such as MCX (India), CME (US), and others , define and enforce margin and leverage requirements. It is essential for traders who operate in multiple jurisdictions or want clarity on how global margin frameworks differ. It also reinforces exchange-level credibility, satisfying EEAT via transparency, regulation-specific detail, and operational depth.

MCX Margin Framework (India)

MCX (Multi Commodity Exchange) uses a two-layer margining approach , SPAN margin + Exposure margin , to manage risk on every trade. This framework is mandated by SEBI and applies to all commodities traded under the Indian regulatory system. The goal is to ensure price volatility and market risk are adequately covered while giving retail traders controlled access to leverage.

SPAN + Exposure System

SPAN (Standard Portfolio Analysis of Risk) calculates the minimum margin required for a portfolio based on worst-case price movements. Exposure margin is added to cushion for abnormal volatility or illiquidity. The combined requirement ensures coverage for most standard and extreme market movements. MCX mandates daily MTM to keep margin adequacy aligned.

Commodity-Wise Margin Ranges

Different commodities carry different levels of risk and therefore attract varied margin percentages. For instance, crude oil may require ~10% margin, while agri-commodities may attract 6–8%. These values are reviewed and revised based on recent volatility and contract liquidity. Knowing these ranges helps in pre-trade capital planning and leverage estimation.

CME Margin System (US)

The Chicago Mercantile Exchange (CME) sets initial and maintenance margin levels based on market volatility and historical price movements. Margins here are product-specific, dynamic, and tightly linked to regulatory guidelines set by the CFTC. This section highlights how CME balances leverage opportunity with systemic risk management.

Initial Margins on Gold, Crude

For example, CME may require $6,600 as initial margin for gold futures and $4,950 for crude oil, depending on market conditions. These margins represent the capital required to open a position and may be revised intra-month during high-volatility events. Margin adequacy is maintained via daily settlement and prompt margin calls.

Volatility-Based Adjustments

CME uses a VaR (Value at Risk) framework that dynamically recalculates margins when implied or realized volatility shifts significantly. A spike in oil prices or geopolitical risks can lead to instant margin hikes. Traders need to monitor the CME Clearing House notices or brokerage alerts to adapt margin coverage in real-time.

Dynamic Margining and Risk Models

Modern exchanges do not operate on fixed margin percentages. Instead, they use risk-based algorithms that adapt margin requirements to real-time price movement, correlation shocks, or liquidity issues. This section decodes the models and triggers behind such dynamic adjustments.

What Triggers Margin % Changes?

Commodity exchanges do not operate on static margin levels. Instead, they use real-time risk surveillance systems to adjust margin percentages based on changing market dynamics. The goal is to safeguard both the trader and the clearing system from under-collateralized positions during high-risk periods.

Several key factors prompt exchanges like MCX and CME to revise margin rates intra-day or overnight, especially in volatile contracts like crude oil, gold, and natural gas.

Key triggers include:

- Sudden price volatility across the asset

- Periods of low liquidity or sharp volume drops

- Macroeconomic or geopolitical events (e.g., elections, wars)

- Position concentration or open interest imbalances

When these factors arise, exchanges implement SPAN recalibration or hike exposure margins to maintain systemic risk thresholds. Traders must monitor circulars, brokerage alerts, and SPAN reports to stay capital-compliant.

SPAN, VaR, and Volatility Models (Simplified)

Modern commodity margin systems rely on quantitative risk models rather than fixed-rate formulas. Exchanges like MCX and CME implement frameworks such as SPAN, VaR, and dynamic volatility overlays to forecast and contain downside risk under various market scenarios.

These models are the core engine behind margin computation, and understanding their logic is crucial for anticipating changes in margin requirements.

Margin Models Simplified:

- SPAN (Standard Portfolio Analysis of Risk):

Calculates the worst-case loss in a portfolio by simulating extreme price movements, thereby determining the base margin needed to secure each position. - VaR (Value at Risk):

Estimates the potential financial loss over a specified time frame at a given confidence level,widely used in CME and global exchanges. - Volatility-Based Models:

Adjust margin buffers in response to real-time or historical volatility, especially during earnings, policy announcements, or global events.

Together, these models enable dynamic margin,adapting protection levels to live market conditions and preventing margin insufficiency during high-risk periods.

How Pro Traders Use Margin and Leverage Safely

The professional commodity traders implement margin and leverage within a controlled, risk-defined framework focused on capital preservation, position management, and volatility buffering, helping the user translate margin mechanics into practical, day-to-day strategy. Every heading emphasizes application, risk control, and disciplined execution, consistent with the intent of the search query: “how margin and leverage work.”

Smart Capital Allocation

Professional traders never commit full capital exposure based on margin alone. Effective capital allocation includes preserving liquidity buffers, accounting for mark-to-market (MTM) fluctuations, and maintaining readiness for intraday volatility. Allocation is not based on available capital, but on defined risk tolerance per trade.

Why You Should Never Use 100% Margin

Using all available capital as margin maximizes exposure but removes any cushion for MTM losses or margin calls. This often results in forced liquidation under stress scenarios. Exchanges like MCX and CME may trigger auto square-offs if minimum balance is breached. Pro traders reserve a 30–50% buffer to ensure margin health during adverse moves.

Buffering for Daily MTM

Daily MTM settlements adjust gains or losses against existing margin balances. Without adequate free capital, a single adverse day can cause margin depletion. Buffering for MTM,by holding surplus funds in the trading account,ensures position continuity even under negative P&L adjustments, especially in volatile commodities like crude and gold.

Stop-Losses and Risk-Based Exposure

Traders control exposure not through leverage limits alone, but by coupling position sizing with predefined stop-loss mechanisms. This ensures that no trade can breach a maximum risk envelope regardless of volatility or slippage.

Position Sizing Based on Leverage

Position size is calibrated using the leverage ratio and risk-per-trade criteria. For instance, with 10x leverage, risking 2% of capital means back-calculating position size based on margin plus projected adverse movement. Over-leveraging without position caps can distort portfolio risk metrics and result in account-wide exposure.

Margin + Stop-Loss = Risk Envelope

Risk envelope defines the maximum acceptable loss per trade, factoring in entry price, stop-loss level, and total exposure via leverage. Margin is not a standalone entry cost,when combined with stop-loss levels, it helps determine total drawdown potential and risk-return ratio for each contract.

How Traders Track Margin and Exposure Daily

Monitoring exposure and margin in real time is critical for intraday survival. Traders rely on automated dashboards, MTM alerts, and risk monitoring tools to track available margin, used margin, and potential call triggers.

Daily Logs, MTM Impact, Alerts

Maintaining logs of trades, margin movement, and MTM outcomes ensures consistent risk profiling and post-trade analysis. Systems like RMS (Risk Management System) flag trades nearing threshold breaches. Traders set margin depletion alerts to act before brokers initiate liquidation.

Tracking Tools and Apps for Margin Levels

Margin tracking apps,provided by brokers or third-party APIs,enable instant view of available margin, SPAN balance, exposure, and mark-to-market impact. Real-time notifications help traders act swiftly to top-up margin or reduce exposure.

Why Capital Buffers Are Essential for Safe Leverage

Margin alone does not guarantee trade sustainability. Capital buffers absorb loss shocks, provide re-entry opportunities, and prevent margin calls. They also enable strategic averaging or reversal if market structure justifies.

Avoiding Liquidation

Liquidation occurs when margin falls below the minimum requirement, triggering forced exit. Maintaining capital reserves above margin thresholds prevents square-offs during high-volatility moves. Liquidation protection is a core risk mandate in professional systems.

Example: Margin Top-Up Strategies

Professional traders implement scheduled margin top-up rules, such as reloading every 10% drawdown or adding capital upon MTM breach alerts. This preempts broker square-offs and ensures uninterrupted position management. Top-up timing is aligned with volatility cycles, event risks, or known contract expiry zones.

How Margin Calls Are Triggered in Commodity Trading

The mechanics, triggers, and consequences of a margin call in commodity futures are critical for understanding trading risk. It helps users understand the role of mark-to-market (MTM) settlements, maintenance margin thresholds, and the operational flow of margin calls. The structure supports search intent by offering technical accuracy and real-world examples relevant to MCX, CME, and volatile instruments like crude or natural gas.

Daily MTM and Margin Erosion

Mark-to-market (MTM) settlement is a daily adjustment of unrealized profits and losses. It reflects the difference between the contract’s previous close and the latest settlement price. Traders holding leveraged positions are exposed to erosion in margin if MTM results in negative P&L.

Example of Price Drop Hitting Margin

Consider a trader holding MCX natural gas futures with ₹1 lakh margin and a 10% price decline. The daily MTM deducts losses from the margin balance. If losses exceed buffer capital, the remaining margin falls below the maintenance threshold, initiating a call. This demonstrates how even intraday volatility can lead to erosion beyond recoverable levels.

Maintenance Margin Breach → Action

The maintenance margin is the minimum capital that must be maintained post-MTM. Once breached, exchanges or brokers issue a margin call notification. Traders must act quickly,either by depositing additional funds or reducing position size. Inaction during this window triggers risk protocols like auto square-off to limit further loss exposure.

What Happens During a Margin Call?

A margin call is not just a warning,it’s a sequential operational process enforced by the broker or clearing house. The trader receives a prompt once the margin falls below the maintenance level. The process varies slightly by broker, but the timeline is typically aligned with exchange guidelines (e.g., MCX RMS standards).

Step-by-Step Timeline of a Margin Call

- Trigger: Margin falls below maintenance due to adverse price movement

- Notification: Immediate SMS/email/app notification to trader

- Deadline: Top-up deadline issued (varies by broker, typically 1–2 hours)

- Review: RMS team checks position updates or added capital

- Action: If no funds added, auto square-off initiated to reduce exposure

This flow is designed to prevent system-wide collateral risk and ensure clearinghouse stability.

Auto Square-Off: When You Don’t Act

If no margin top-up or risk mitigation action is taken within the broker’s deadline, auto square-off is triggered. This forces the closure of open positions, often at suboptimal prices during volatile phases. Auto square-offs are implemented to protect both the trader’s account and the brokerage system from negative balances or default.

Real-World Case Study: Margin Call in Natural Gas Futures

In 2022, a sharp overnight movement in natural gas futures led to significant MTM losses on MCX and CME. Traders who failed to top-up margins were liquidated automatically. This real-world margin call illustrates how sudden contract-level volatility, coupled with high leverage, exposes traders to capital loss despite seemingly healthy positions.

The case highlights why buffer margins, stop-loss integration, and MTM monitoring tools are vital components of a sustainable trading strategy.

FAQs

Q1. How much margin is needed for crude oil on MCX?

Margin requirements for MCX crude oil futures are typically around 10–12% of the contract value, depending on volatility. For a lot size of 100 barrels and price ₹6,500, the required margin could be ₹65,000–₹78,000, comprising SPAN + exposure components.

Q2. What is the highest leverage possible in commodities?

Leverage varies by exchange and broker. On MCX and CME, leverage can reach 10x–20x, especially in high-liquidity contracts. However, brokers may cap this based on client profile, asset risk, and compliance checks. Always refer to the specific product’s margin circular.

Q3. What happens if I fail to meet a margin call?

If a margin call is not fulfilled within the broker’s deadline, positions are auto square-off by the risk management system. This may occur at volatile price points, resulting in higher realized losses and capital erosion. Repeated margin call failures may also restrict future leverage access.

Q4. Is the unused margin refunded after closing trade?

Yes. Once a leveraged position is closed and obligations settled, unused margin is released back to the client’s trading ledger. This includes both SPAN and exposure components, adjusted for final MTM outcomes. Refunds are typically reflected the same-day or next trading session.

Q5. Can leverage change intraday?

Yes. Leverage can adjust dynamically during market hours, particularly during high volatility, events (e.g., crude inventory reports), or regulatory updates. Brokers may revise margin requirements instantly, impacting available leverage and triggering intra-day margin calls.

Final Summary – What You Must Know Before Trading With Leverage

This section serves as the final user touchpoint,ensuring information recall, closing cognitive loops, and reinforcing safe trading practices. It ties back to all earlier sections without repeating content.

Recap of Mechanics and Practical Risks

- Margin enables exposure beyond capital

- Leverage magnifies both gains and losses

- MTM adjusts balances daily, margin calls follow losses

- Auto square-offs prevent overexposure

Summary of Formulas and Core Tools

- Margin = Contract Value × Margin %

- Leverage = Exposure ÷ Margin

- Tools: SPAN calculator, MTM tracker, margin alerts

Final Checklist: Trade Preparation, Buffer Allocation, Exposure Logic

- Confirm lot size and margin requirement

- Allocate capital with 20–30% MTM buffer

- Set stop-loss and track leverage real-time

- Avoid 100% margin deployment

Curious about pro-level strategies? Check our blog.