Python is a high-level programming language, and its simplicity makes it ideal for building and scaling algorithmic trading systems, automated execution, real-time data handling, and integration with broker APIs without excessive complexity.

Libraries like Pandas, NumPy, yFinance, and Backtrader streamline everything from data processing to strategy testing and order execution, reducing development time while increasing precision and control.

Python supports traders across all levels, allowing them to automate signals, monitor performance, and adapt to evolving market conditions,and remains the most effective tool in modern algorithmic trading workflows.

Why Python Is the Go-To Language for Algo Trading

Python is the standard choice for algorithmic trading because of its rapid development time, reduces complexity, debugging and works seamlessly across environments(various machine), Its concise syntax eliminates unnecessary boilerplate, allowing traders to focus on logic and strategy rather than code structure, all critical when speed, precision, and adaptability define your trading edge.

For practical use:

- Build and test strategies faster using Pandas (data manipulation), NumPy (numeric computation), and TA-Lib (technical indicators).

- Run error checks and debug live strategies quickly using built-in IDE tools and clean exception handling.

- Backtest reliably with libraries like Backtrader, PyAlgoTrade, and Zipline—customizable and broker-agnostic.

- Deploy anywhere, code runs consistently across Windows, macOS, Linux, or cloud VMs with minimal setup.

- Connect to brokers and exchanges via Python-compatible APIs (Zerodha Kite, Interactive Brokers, Binance).

- Visualize performance using Matplotlib or Plotly, helping traders review, refine, and optimize based on data.

What You Need to Get Started with Python (No Experience Required)

You don’t need a finance degree or prior coding experience to begin algorithmic trading with Python. You do need clarity on foundational concepts and the right tools to build and test your strategies from day one.

Prerequisites

A solid foundation is required before implementing algorithmic trading strategies using Python:

- Trading Fundamentals:

Basic knowledge of how markets function, including order types such as market, limit, and stop-loss, is essential. Understanding strategic models like momentum, mean reversion, and breakout trading forms the logic layer behind most automated systems. - Python Programming Basics:

Familiarity with Python syntax, control structures (loops, conditionals), and function definitions enables algorithm development. These concepts can be learned alongside practical applications using beginner-friendly resources such as open-source notebooks, tutorials, and documentation. - Data Handling Skills:

Working with structured financial data is critical. This includes reading and manipulating time-series datasets (CSV, API data), applying calculations for indicators, and visualizing trends. Libraries such as Pandas, NumPy, and Matplotlib provide efficient tools for managing these operations.

Establishing these foundations ensures readiness to progress from theoretical knowledge to hands-on strategy design and execution in an algorithmic trading workflow.

Tools to Install

A proper development environment is necessary to build, test, and deploy algorithmic trading strategies:

- Python Installation:

Use Anaconda for a complete, bundled environment that includes popular data science libraries and Jupyter support. Alternatively, install vanilla Python from python.org for a leaner setup and configure dependencies manually as needed. - Integrated Development Environment (IDE):

Start with Jupyter Notebook for an interactive coding interface that simplifies testing, visualization, and prototyping. For modular development, version control, and plugin support, opt for Visual Studio Code (VS Code). - Python Package Installer (pip):

Pre-installed with Python, pip is used to install and manage external libraries like pandas (data analysis), numpy (numerical computing), matplotlib (charting), and yfinance (financial data access). Ensure all packages are up to date using pip install –upgrade.

Establishing these tools ensures a reliable local environment for building efficient, testable, and scalable trading systems.

Where to Install and Set Up:

Option 1: Easiest – Install Anaconda (Recommended for Beginners)

Where to install:

- Visit https://www.anaconda.com

- Download and install for Windows, macOS, or Linux

Why this is ideal:

- Anaconda includes Python, Jupyter Notebook, pip, and pre-installed libraries like numpy, pandas, and matplotlib.

- No separate setup is needed.

- Ideal for running trading experiments quickly in Jupyter.

Option 2: Manual Install (If You Prefer a Lightweight Setup)

Step-by-step (for Windows/macOS/Linux):

- Install Python from https://www.python.org/downloads

- During installation, check “Add Python to PATH”

- Install pip (comes built-in with modern Python)

- Install an IDE:

- VS Code: https://code.visualstudio.com/

- Or install Jupyter Notebook via pip

Essential Python Libraries for Algorithmic Trading

To build functional and scalable algorithmic trading systems in Python, traders rely on a mix of data handling, financial data APIs, and backtesting libraries.

Below is a categorized breakdown of libraries you need to master.

Data & Analysis

These libraries form the backbone of data ingestion, transformation, and visualization workflows.

- Pandas: A powerful library for handling time-series and structured tabular data. It enables data cleaning, slicing, and custom indicators—critical for developing rules-based strategies.

- NumPy: Provides fast array computations and vectorized operations. It’s essential for signal processing, matrix math, and performance optimization in high-frequency systems.

- Matplotlib: Enables customized data visualization. You can plot candlestick charts, moving averages, and strategy performance, making debugging and validation more transparent.

Financial Data

These APIs fetch real-time and historical price data—an essential input for any algorithm.

- yFinance: A simple wrapper to download historical stock and ETF data from Yahoo Finance. It’s widely used for quick prototyping and backtesting equity-based strategies.

- Alpha Vantage: Offers time-series data for equities, forex, and cryptocurrencies. It also supports technical indicators out-of-the-box, making it ideal for signal research and cross-asset trading.

- CCXT: A unified cryptocurrency exchange API. It allows algo traders to fetch live order books, execute trades, and collect tick-level data across dozens of crypto exchanges.

Backtesting & Strategy Development

These libraries simulate your trading logic on historical data to measure profitability, drawdowns, and risk.

- Backtrader: A widely adopted framework that supports both backtesting and live trading. Its modularity makes it suitable for both beginners and professionals building multi-indicator systems.

- Zipline: Designed for equity strategies, Zipline handles event-driven backtesting using minute or daily bars. It’s great for clean, research-oriented workflows.

- QuantConnect: A cloud-based backtesting and live-trading environment that supports stocks, futures, forex, options, and crypto. It’s useful for professional deployment, collaborative development, and leveraging institutional-grade datasets.

Learn by Doing: Build Your First Algo in Python

The best way to understand algorithmic trading is to build a basic trading bot using real data. Below is a simplified step-by-step example that introduces you to the core workflow, from data fetching to backtesting.

Note: This example is meant for learning purposes only.

Step-by-Step Example

1. Fetch stock data using yFinance

Use the yfinance library to download historical stock data (e.g., for AAPL). It returns clean time-series data that can be directly used for analysis.

2. Add a simple indicator: Moving Average

Calculate a 20-day moving average to identify short-term price trends.

3. Define basic buy/sell logic

Create signals: Buy when price crosses above MA20, sell when it crosses below.

4. Backtest with Pandas or Backtrader

For simplicity, use Pandas to calculate returns and visualize performance. If you’re ready, shift to Backtrader for more detailed strategy testing and broker simulation.

How to Backtest Strategies with Python

Backtesting is the process of evaluating a trading strategy using historical data to see how it would have performed in the past. It helps determine whether your algorithm is effective before risking real money. A solid backtest reveals if your logic holds up across different market conditions, and highlights metrics like profit, risk, and consistency.

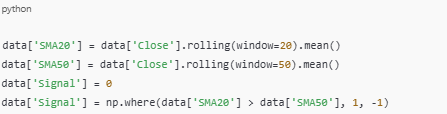

Example: Backtest a Simple SMA Crossover Strategy

Objective:

Buy when a short-term moving average (e.g., 20-day) crosses above a long-term average (e.g., 50-day), and sell when it crosses below.

Backtest Logic:

Calculate returns based on these signals and compare them with the asset’s actual performance.

Validate Performance with Key Metrics

Performance evaluation is essential before live deployment. Use the following metrics to assess the effectiveness and risk profile of any strategy:

- PnL (Profit and Loss):

Calculates the net return over the backtest period. Indicates overall profitability but must be interpreted alongside risk metrics for full context. - Sharpe Ratio:

Quantifies return per unit of risk by comparing excess returns to standard deviation. A higher Sharpe Ratio signals better risk-adjusted performance, essential for sustainable strategies. - Maximum Drawdown:

Measures the worst historical decline from peak to trough. Highlights vulnerability to losses and helps determine appropriate position sizing and stop-loss placement.

These metrics should guide strategy selection, refinement, and deployment readiness. Poor results in any area require further backtesting, parameter tuning, or rethinking the logic before moving forward.

Going Live – How to Deploy Your Python Strategy

Once your strategy performs well in backtests, the next step is deployment—executing trades automatically through a broker’s API. This means connecting your Python code to a real trading account to place, monitor, and manage orders without manual input.

Connect with a Broker’s API

To deploy your Python trading algorithm live, you must connect it with a broker’s trading API that supports programmatic access to market data and order execution. Choose a broker based on your region, asset class, and ease of integration:

- Zerodha Kite Connect (India) – Offers REST APIs with solid documentation and reliability. Paid access is required, but it’s widely used in the Indian retail trading space.

- Alpaca (U.S.) – Commission-free equities trading with a fully open, developer-friendly API. Ideal for testing and live deployment without fees.

- Interactive Brokers (Global) – Supports a broad range of asset classes (stocks, options, futures, forex). More complex to integrate but powerful for advanced traders.

Install broker SDKs (e.g., kiteconnect, alpaca-trade-api) and authenticate using API keys.

Handle Order Placement and Monitoring

Your algo must convert trading signals into actual orders with robust handling:

- Use SDK methods to place market, limit, or stop-loss orders:

kite.place_order(tradingsymbol=”INFY”, transaction_type=”BUY”, order_type=”MARKET”, quantity=1)

- Monitor order status, fill confirmation, and modify or cancel orders in real time based on execution status.

- Implement error handling, retry logic, and logging to detect failures, avoid duplicate orders, and maintain execution reliability.

- Use scheduled jobs or WebSocket streaming to trigger decisions without polling delays.

By integrating your algorithm with a broker’s live API, you bring your strategy into production while retaining full control over logic, timing, and capital allocation.

Tips for Learning Faster and Smarter

If you’re serious about mastering Python for algorithmic trading, the key is to learn by doing, not just reading. These practical tips will accelerate your progress and help you build confidence with real-world exposure.

Learn by Copying and Modifying Real Code

Clone open-source repositories (e.g. SMA/EMA strategies on GitHub).

Don’t just run them, trace each line, understand what every function does, then rewrite it from scratch using your own logic.

Change variables, timeframes, or assets to test how strategies behave. This builds true comprehension, not just repetition.

Join Active Developer-Trader Communities

Integrate yourself into Python + trading circles:

- Reddit (r/algotrading) for exposure to practical problems and working solutions

- Discord communities for real-time help on strategy logic or API integration

- StackOverflow for solving Python bugs quickly

These platforms expose you to real workflows, edge cases, and tools professionals use.

Build Micro Projects with Real Objectives

Set up structured micro-goals:

- Pull live data with yfinance or ccxt

- Apply and visualize one technical indicator

- Define a buy/sell logic and simulate outcomes

Each mini-project should teach one skill: data ingestion, signal generation, or backtesting logic. Stick to short iterations—avoid large, complex systems early on. This approach compounds into real trading systems faster.

FAQs

Can I do algo trading with zero coding experience?

Yes, many platforms today offer no-code or low-code solutions (like TradingView, AlgoTest, or QuantConnect templates). But learning Python gives you full control over strategy customization, automation, and backtesting—making it a long-term advantage.

How long does it take to learn Python for algo trading?

If you study consistently, you can learn basic Python and build your first trading bot within 4–6 weeks. Focus on key areas: data handling (Pandas), logic building (if-else, loops), and reading API docs.

Is Python enough, or do I need other tools too?

Python is the core language, but you’ll also use tools like:

- Broker APIs (e.g. Zerodha Kite Connect, Alpaca)

- Backtesting frameworks (Backtrader, Zipline)

- Data sources (yFinance, Alpha Vantage)

These are libraries or services that integrate seamlessly with Python.

What’s the best way to practice safely?

Always start with paper trading or backtesting. Use historical data to test your strategies before risking real money. Platforms like Backtrader or TradingView let you simulate trades with zero capital risk.

Final Thoughts

Python will remain a go to code in Algorithmic Trading; its integration with machine learning, cloud computing, and big data analytics will unlock more intelligent, adaptive trading models.

From real-time signal processing to predictive forecasting and automated risk management, Python enables faster development, smoother debugging, and easier scaling, giving flexibility to build smarter strategies over time.

Whether you’re a beginner or advancing toward professional-grade systems, Python will continue to be efficient, high-impact trading workflows.

Master new trading techniques on our blog.