Quantitative trading offers a systematic alternative. It uses data pipelines, mathematical rules, and automated execution systems to transform market information into consistent, repeatable decisions. Instead of guessing, traders rely on code, statistical structure, and software-driven workflows that operate with precision.

Prices react in milliseconds, liquidity shifts across venues, and information flows through dozens of channels at once. In this environment, traditional discretionary decision-making struggles to keep pace and quantitative trading provides a decisive edge.

This article explains what quantitative trading is, why it drives modern markets, and how it operates across major institutions. It outlines the workflow from data ingestion to modelling, backtesting, execution, and monitoring, and shows how software, AI, ML, and LLMs solve key research challenges and shape the future of systematic trading.

Table of Contents

Why Does a Modern Trader Need Quantitative Trading?

Quantitative trading provides a modern trader with a deterministic, software-driven structure for analysis, signal generation, and execution. Quantitative trading delivers advantages in precision, speed, consistency, scalability, and risk control under data-intensive market conditions.

| S.No. | Benefit | Description |

|---|---|---|

| 1 | Precision | When statistical models convert structured datasets into rule-based signals. |

| 2 | Consistency | When every trade follows predefined computational logic. |

| 3 | Speed | When automated engines evaluate real-time market conditions at sub-second intervals. |

| 4 | Risk Control | When workflows enforce position limits, volatility filters, and execution constraints. |

| 5 | Scalability | When systems operate across multiple instruments, markets, and timeframes. |

| 6 | Strategy Stability | When backtested rules replicate historical behavior in live data. |

Quantitative trading provides structural advantages in markets defined by high data volume, fragmented liquidity, and rapid microstructure changes and it also supplies a complete operational workflow that links research, execution, and monitoring.

| S.No. | Category | Quantitative Trading Advantages |

|---|---|---|

| 1 | Support Analysis | It interprets order-flow variables, volatility regimes, and cross-asset relationships with statistical accuracy. |

| 2 | Support Execution Behaviour | It aligns execution behavior with latency conditions, slippage characteristics, and order-book dynamics. |

| 3 | Support Research | Research tasks with Python environments, data pipelines, feature-engineering tools, and validation procedures. |

| 4 | Support Execution | Execution tasks with APIs, routing algorithms, and automated fill-processing logic. |

| 5 | Support Monitoring | Monitoring tasks with dashboards, performance logs, and risk-reporting systems. |

Quantitative trading matches the technological direction of modern financial markets, where automation, data-centric analysis, and low-latency infrastructure determine competitive performance.

Quantitative trading ensures that a modern trader maintains accuracy, repeatability, and computational reliability under evolving market conditions.

QUANTITATIVE TRADING — ADOPTION AND USAGE

Quantitative trading operates across the full financial ecosystem and supports institutional and retail market participants. Quantitative trading expanded from hedge-fund and investment-bank environments into quant-focused funds, proprietary trading desks, global exchanges, and retail trading platforms. Quantitative trading uses specialized hardware and software ecosystems developed by major technology firms.

| Quantitative Trading Use Case Examples: | Quantitative Trading Implementations: |

|

|

Quantitative trading integrates artificial intelligence (AI), machine learning (ML), and large language models (LLMs) into operational research and model-development processes.

- Quantitative trading uses ML algorithms to detect structural patterns, evaluate regime shifts, and estimate predictive signals.

- Quantitative trading uses LLM-assisted research tools and cloud-based simulation environments to test ideas, optimize model parameters, and increase research throughput.

- Quantitative trading benefits from academic programs, including quantitative-finance curricula at institutions such as the Wharton School, that support standardized training and industry adoption.

Quantitative trading has become a foundational component of modern financial infrastructure because software-driven research, data-centric execution, and automated risk systems define current market practices.

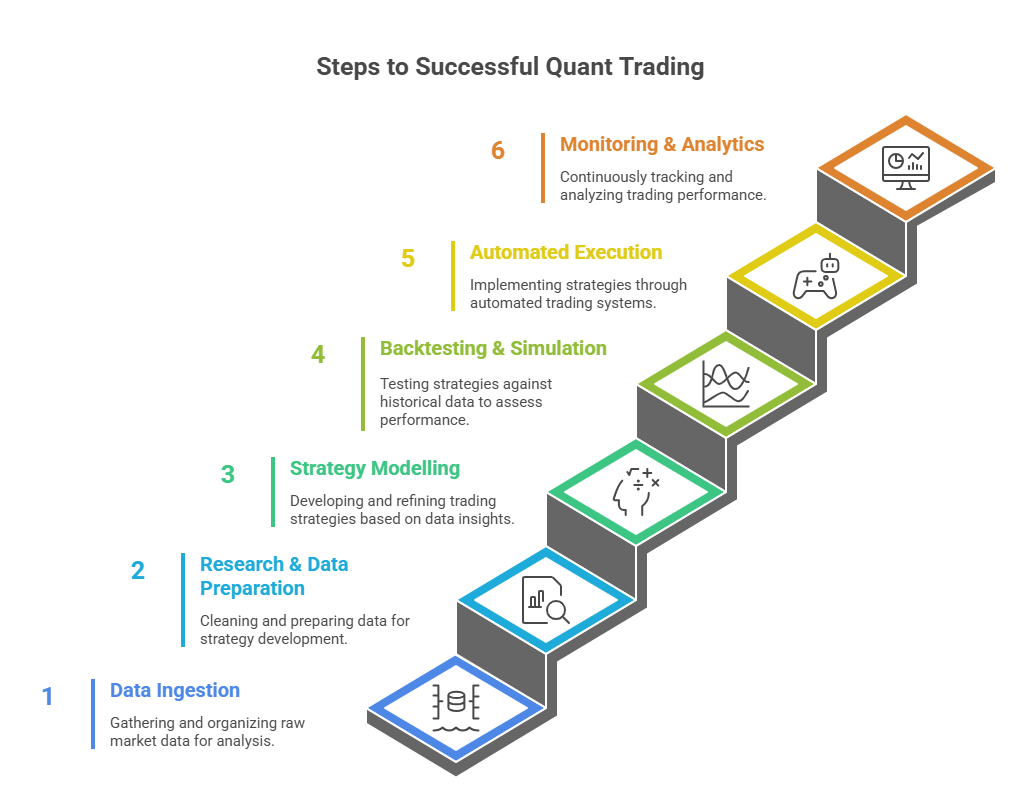

How Quant Trading Works: The Modern Software Workflow

Quantitative trading runs on a structured, software-driven workflow where every stage—data, research, modelling, testing, execution, and monitoring—is automated and reproducible. The process moves through a series of tightly connected steps as follows and below will be the explanation for each:

1. Data Ingestion

2. Research & Data Preparation

3. Strategy Modelling

4. Backtesting & Simulation

5. Automated Execution

6. Monitoring & Analytics

1. Data Ingestion

Quantitative trading begins by collecting market data from multiple sources such as real-time price feeds, historical datasets, fundamentals and news, sentiment and alternative data, exchange-level order-flow information.

APIs and vendor feeds supply continuous streams of data that form the raw input for strategy development.

2. Research & Data Preparation

Once data is collected, it enters a research environment—usually Python, Jupyter notebooks, or LLM-assisted tools. Here, traders clean and normalise datasets, handle missing values and adjustments, visualise patterns and correlations, engineer features that become trading signals. This step transforms raw inputs into structured, analysis-ready information.

3. Strategy Modelling

With prepared data, traders build models that define how trades are triggered. Techniques include statistical indicators, factor models, machine-learning pipelines, custom mathematical rules. The goal is to convert observed patterns into repeatable, rules-based logic.

4. Backtesting & Simulation

Models are tested inside a backtesting engine that simulates realistic market conditions such as slippage and transaction costs, latency and execution delays, order-book behaviour, liquidity constraints. Years of market data can be simulated in minutes, allowing traders to identify strengths, weaknesses, and edges.

5. Automated Execution

When a strategy passes testing, it is deployed into an execution system using REST or FIX APIs. These systems send orders automatically, route trades across brokers and exchanges, manage fills and rejections, enforce risk limits in real time, execution infrastructure ensures the strategy behaves exactly as designed.

6. Monitoring & Analytics

Live strategies are continuously observed through dashboards and logs, real-time PnL curves, risk and exposure metrics, automated alerts and fail-safes. Monitoring ensures the system remains stable, accurate, and aligned with market behaviour.

SKILLS & TOOLS USED IN QUANTITATIVE TRADING

Quantitative trading requires a combination of technical skills and software tools that support data processing, model development, backtesting, execution, and monitoring. These competencies form the operational foundation that allows a trader to build, test, and deploy systematic strategies with reliability and precision.

Core Skills Required in Quantitative Trading

A modern quant develops a skill set that blends programming, statistical reasoning, and market understanding. These skills allow traders to convert raw data into predictable, rules-based trading logic.

Essential skills include:

- Python programming for research workflows, data manipulation, and strategy modelling.

- Statistics and probability for understanding distributions, correlations, volatility, and hypothesis testing.

- Machine learning fundamentals for classification, regression, feature engineering, and model validation.

- Market microstructure awareness to understand order types, liquidity, slippage, and execution mechanics.

- Backtesting and simulation design to evaluate strategies under realistic constraints.

Together, these skills ensure that quantitative trading systems are built on a structured, analytical, and reproducible foundation.

Software Tools Used in Quantitative Trading

Quantitative trading relies on tools that automate each stage of the research and execution workflow. These tools make strategy development faster, more consistent, and more scalable.

Key tools include:

1. Programming environments (Python, C++): Python supports research and prototyping, while C++ powers latency-sensitive execution engines.

2. Backtesting engines (QuantConnect, Backtrader, Zipline): These platforms simulate historical performance with realistic fills, slippage, and costs.

3. Execution APIs (Interactive Brokers API, MT5, cTrader, FIX): APIs connect quantitative-trading algorithms to real markets through automated order routing.

4. Data platforms (market-data vendors, real-time feeds, alternative datasets): These supply price data, fundamentals, sentiment, and microstructure signals used to generate trading inputs.

5. Cloud compute (AWS, GCP, Coiled): Cloud systems scale backtests, store large datasets, and run parallel optimization workloads.

6. AI and LLM tools (code assistants, feature-engineering helpers, research accelerators): These tools streamline data cleaning, automate modelling tasks, and generate structured research templates.

Why These Skills and Tools Matter

Quantitative trading depends on reproducible workflows. The right skills allow traders to build those workflows; the right tools allow them to deploy them at scale. Together, they transform trading from a discretionary activity into a software-driven process that adapts to modern market conditions.

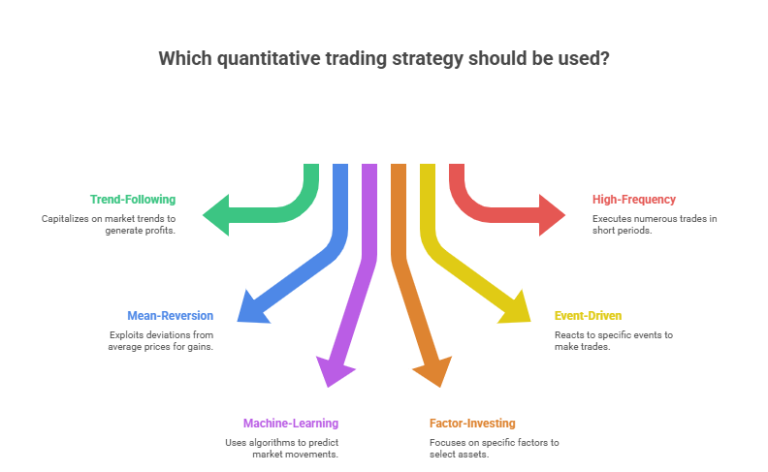

Strategies Used In Quantitative Trading (With Real Examples)

Quantitative trading uses systematic strategies built on statistical rules, predictive models, and algorithmic decision frameworks. These strategies transform market data into actionable signals and use software systems to execute trades consistently across different market conditions.

Below are the major strategy categories, how they work, why traders use them, and real-world software applications.

1. Trend-Following Strategies

2. Mean-Reversion & Pairs-Trading

3. Machine-Learning–Based Models

4. Factor-Investing Strategies

5. Event-Driven Strategies

6. High-Frequency Microstructure Strategies

| 1. Trend-Following Strategies | |

| Trend-following strategies identify sustained price movements and trade in the direction of momentum. | |

| How it works: | Why traders use it: |

|

|

| Software use-case: | Beginner-friendly example: |

|

|

| 2. Mean-Reversion & Pairs-Trading | |

| Mean-reversion strategies assume that prices or spreads return to their historical averages. | |

| How it works: | Why traders use it: |

|

|

| Software use-case: | Beginner-friendly example: |

|

|

| 3. Machine-Learning–Based Models | |

| ML strategies analyze complex patterns in historical data to forecast price direction, volatility, or market regimes. | |

| How it works: | Why traders use it: |

|

|

| Software use-case: | Beginner-friendly example: |

|

|

| 4. Factor-Investing Strategies | |

| Factor strategies build portfolios based on statistical characteristics rather than subjective selection. | |

| How it works: | Why traders use it: |

|

|

| Software use-case: | Beginner-friendly example: |

|

|

| 5. Event-Driven Strategies | |

| Event-driven strategies trade around scheduled or news-driven catalysts. | |

| How it works: | Why traders use it: |

|

|

| Software use-case: | Beginner-friendly example: |

|

|

| 6. High-Frequency Microstructure Strategies | |

| HFT strategies operate at microsecond speed and rely on order-book dynamics. | |

| How it works: | Why traders use it: |

|

|

| Software use-case: | Beginner-friendly example: |

|

|

Why Do These Strategies Matter?

Quantitative trading strategies convert market behavior into structured rules that can be tested, optimized, and executed automatically. Each strategy type serves different market conditions, enabling traders to create diversified, adaptive, and scalable trading portfolios.

Challenges Traders Face and How Software Solves Them

Quantitative trading encounters structural challenges that affect data quality, simulation accuracy, model robustness, execution reliability, and system oversight. Quantitative trading resolves these challenges with software systems that create consistent, repeatable, and production-ready workflows.

1. Dirty or inconsistent data: Data problems like missing fields, wrong corporate-action adjustments, and timestamp mismatches can weaken signals. In quantitative trading, these issues are fixed with automated cleaning pipelines that standardize variables and align time-indexed records. Once preprocessing rules correct these errors, the strategy works with cleaner and more reliable inputs.

2. Slow or unreliable backtesting: Backtests can feel slow when simulation engines use outdated or inefficient methods. To support quantitative trading at scale, optimized frameworks rely on vectorized operations and distributed computing that speed up multi-year tests. This makes research faster and gives traders predictable, stable backtest results.

3. Overfitting in models: Models sometimes learn noise instead of genuine market structure, creating unstable behaviour. In quantitative trading, this is controlled through walk-forward validation, cross-validation, and out-of-sample testing that reveal weaknesses early. These steps help models generalize better and perform more reliably in live markets.

4. Slippage and latency issues: Executions can drift from quoted prices or react slower than market movements, creating slippage. Since execution quality matters in quantitative trading, faster broker APIs, routing logic, and slippage-estimation tools help strategies react on time. This alignment improves execution accuracy and makes backtests closer to real-world conditions.

5. Monitoring fatigue: Constant supervision becomes tiring when strategies run all day and react to fast market changes. For quantitative trading teams, automated alerts, structured logs, and rule-based risk tools reduce the need for manual oversight. These systems keep trading stable and cut down on continuous monitoring.

The Rise of AI, ML, and LLMs in Quantitative Trading

1. Quantitative trading uses artificial intelligence (AI) to increase the precision, speed, and consistency of research workflows.

- It uses machine learning (ML) models to classify market regimes, detect structural anomalies, and measure signal persistence.

- It uses large language models (LLMs) to convert research inputs into executable code.

Together, these systems reduce modelling errors, shorten iteration cycles, and standardize analytical procedures.

2. Quantitative trading applies AI-driven feature engineering to create volatility metrics, microstructure variables, and sentiment-based factors.

- It uses ML pipelines to optimize hyperparameters, validate predictive performance, and test out-of-sample robustness.

- It uses LLM frameworks to summarize academic papers, extract formulas, and clarify methodological assumptions.

3. Quantitative trading accelerates research throughput with natural-language query tools that retrieve factor evidence, dataset properties, and structural relationships.

- It evaluates computational performance with hardware-optimized benchmarks.

- For example, STAC’s 2023 STAC-M3 results demonstrated significant improvements in simulation latency and backtest throughput.

These advances feed directly into large-scale simulations, walk-forward tests, and portfolio stress-evaluations.

4. Quantitative trading reduces operational overhead through generative-AI systems that detect coding inconsistencies, create diagnostics, and automate repetitive modelling tasks.

- It improves pipeline stability with structured code suggestions, automated documentation, and standardized research templates.

- It increases strategy durability by monitoring data drift, signalling degradation, and parameter sensitivity.

Quantitative trading ultimately integrates AI, ML, and LLMs as research accelerators—not autonomous decision-makers—creating reproducible workflows, consistent outputs, and measurable improvements across the full strategy-development lifecycle.

Conclusion: Quant Trading Is a Software-Driven Discipline

Quantitative trading replaces discretionary decision-making with structured workflows built on data, mathematical rules, and automated execution. As markets evolve toward higher speed, greater complexity, and heavier data flow, systematic approaches provide the precision, consistency, and scalability that traders need to remain competitive.

Software-driven solutions address challenges in data quality, simulation accuracy, model robustness, and execution reliability, ensuring that strategies behave predictably in both research and live environments.

With the rise of AI, machine learning, and LLM-assisted research, quantitative trading continues to expand in capability and efficiency. These technologies accelerate analysis, reduce development cycles, and enhance the stability of systematic models.

At its core, quantitative trading is not just a technique—it is an operating discipline. Traders who adopt structured, software-powered methods gain the ability to design strategies with clarity, scale them with confidence, and adapt them as markets change.

Learn how top traders operate, explore our blog.